Why Trust Matters More Than Innovation in FinTech!

.jpeg)

.avif)

Introduction

In this episode of Building Momentum, Yash sits down with Pallavi from PCA Global Associates to unpack how FinTech is evolving across geographies, and why trust, compliance, and discipline matter more than speed alone.

Pallavi shares insights from working across financial services, embedded finance, challenger banking, and global regulatory ecosystems, highlighting a crucial mindset shift for founders and product leaders: innovation without trust doesn’t scale.

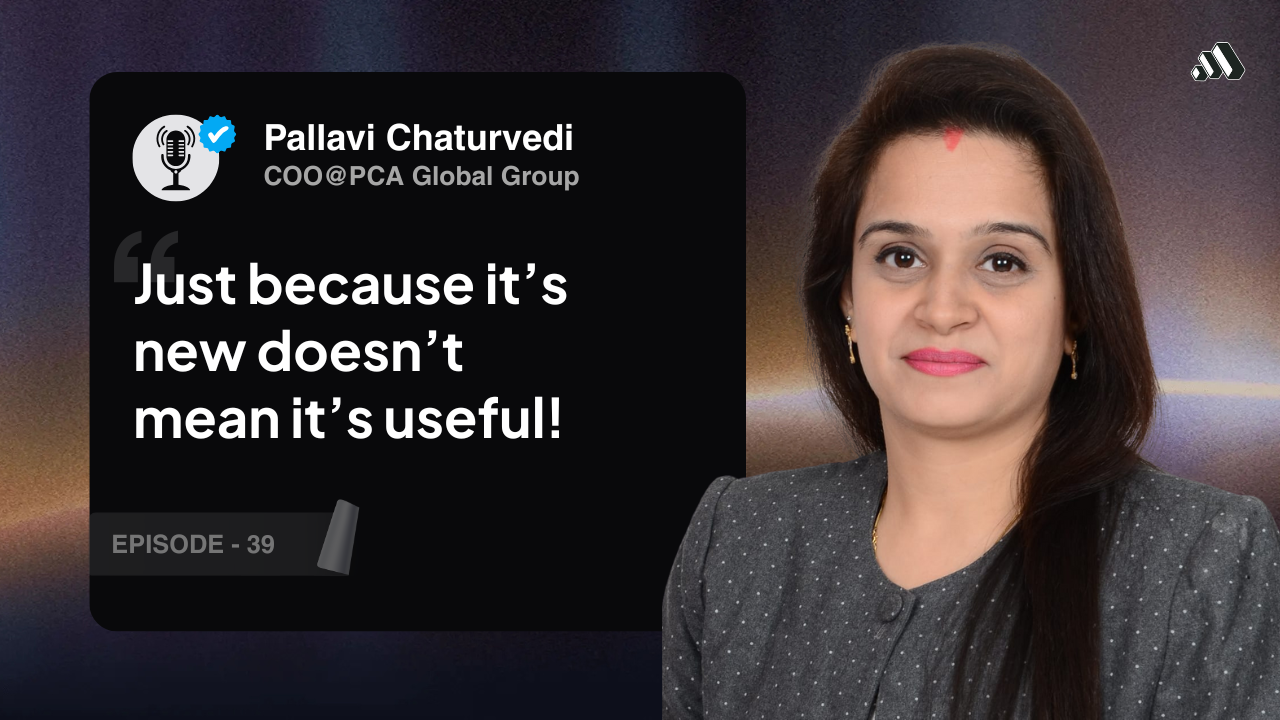

"It’s important to build trust first, innovate second."

- Pallavi Chaturvedi

Key Takeaways

- PCA Global Group is a diversified company involved in various sectors.

- Building trust is essential for innovation in financial services.

- Regulatory compliance is crucial for successful product development.

- FinTech trends vary significantly across different regions.

- Embedded finance is transforming customer experiences.

- Tokenization and CBDCs are key trends in the financial sector.

- Operational security is as important as data security.

- Super apps are emerging as a significant trend in fintech.

- Speed and discipline are critical for building trust.

- Innovation must address real problems to be effective.

Transcript

Hello and welcome to Building Momentum. Today we are in conversation with Pallavi from PCI Global Associates. We are not just the leaders, we are the bridge. Even the biggest of empires can get crashed over just to us. Indian business models are now completely dependent on our UPS implementation. If I take out a debt, then the NBFC or whoever is given the debt is able to deduct it directly from my future salary.

Who does this industry belong to? So, to my understanding Generally we end up starting with innovation It's important to build trust first, innovate second

name is Yash, your host of the show. And today we are in conversation with Pallavi from PCA Global Associates. Today we talk about a lot of innovation in the financial services and fintech sector, starting from challenger banking to embedded finance and to asset tokenization as well. We also talk about building trust and maintaining a balance between innovation and trust, and then also the difference between innovation and usefulness.

I hope you will find value from this conversation and if you like it then do consider subscribing as well. Hey Pallavi, thank you for doing this. Before we begin, could you share with us a little bit about PCA Global Associates?

Suddenly, thank you, Yash, for calling us over. PCA Global is basically a very diversified company. We have evolved and emerged ourselves into IT-based services with FinTech, Edutech, and HealthTech. And now we are also stepping up into energies, green energies. So market has always been evolving us into different shapes.

even giving us opportunities to dig into different segmentation of the world. That's how we are basically diversified into. And if I say about myself,

I basically evolved from an engineering background and then transformed into a tech leading organization over 20 years. I had experienced with IT segmentation into all of the sectors that we had served on to and then finally co-founded PCA Global. And now I am leading the operations and strategic partnership along with the organization. So yes, we have got deeper goals.

meaningful roadmaps that we had defined. even in this ever turning, ever emerging IT trends, we always prefer to look forward to have futuristic approach, not just developing a product, but also solving a major problem.

So we are into, I'm into basically mentoring founders as well, helping them scale up their products for the global market, understanding the responsibility, resilience, as well as the upcoming trends that can keep them at least a couple of steps ahead of what's already going on to the market. Because if you have been a little more futuristic, that is going to bring your product more workable with the clients.

with governments, with enterprises and all. So to us, we are not just the leaders, we are the bridge. We build bridge between product and regulators. We are building bridges between innovation and operational deliveries. And we are building bridges between local markets, local developers, local products with global markets.

So that's actually one of the reasons of having you here, right? So one of the things that really attracted us to inviting you on the show was that it's extremely diversified, as you also rightly pointed out, like financial services, healthcare, like multiple different sectors that you work in. What is that one common thread or one sort of challenge that you see that, you know, doesn't matter what industry that after a certain

scale, whatever industry it is, this as a challenge is yet to be solved. So challenges are everyday emerging. It's not that one thing that you will point it out to solve and that's what you're supposed to achieve, right? It's an everyday course of action.

We know the internet, the green side, the dark side, as well as the white side where we all are working. So as we are doing more responsible, more compliant work towards either of the segmentation, whether it is the FinTech, Agitech, or HealthTech, so has been on the other side of the IT as well. So it's essentially and evidently important for us to make sure that we are compliant enough.

building the trust. Now trust doesn't come overnight or doesn't stays overnight too. Even the biggest of empires can get crushed over trust. So it's extremely extremely important to maintain that trust and that needs a lot of effort, extreme discipline and very niche roadmaps for the innovations that we are doing.

So, would it be fair to say that staying compliant and consistently being able to maintain or raise the level of trust is something that as a major challenge you've seen across all the sectors wherever you're offering solutions. that be fair? Absolutely. Absolutely. So, in a crux, you can say that it's important to build trust first, innovate second.

Generally, we end up starting with innovation. We end up thinking, how are we different? What should we build new? Now that I think about it, I agree to this more, that if you have the trust, then you can do a lot of other things as well and scale the company. building, like if the mindset from day one, as I think about my own journey as well, if the mindset on day one is,

if I perform this action, if I introduce this policy, if I create this as a contract, if I, whatever, right? Any action that I do, if my mindset is, will this build more trust or will this erode trust? And then I consistently end up doing things that will build more trust. And that would make my company stronger for sure. And would have been stronger if that had been the mindset. So.

So specifically coming to the financial services as a sector where you've been working in for a while, can you talk us through some major milestones that you've accomplished in the sector? Okay, so- Major deliveries, like something that you're, you know, there are those things that you're proud of.

We didn't think we could, but we did. Okay, so FinTech is not just related to one product. It's purely based on the client's expectations. And this all revolves around a business purpose. So there had been many. I won't pin out to one because that would be unfair to other segmentation. So to me, every single delivery has been

extremely commendable. But the appreciation has been with my team, our leadership intends.

and definitely our delivery disciplines that we had maintained so far. And even a very strict understanding by that we are delivering into any of the countries that we are working. We are basically not doing too much into the domestic front. Our focus is on the export segmentation. So we are very much strong, clear, and reasonable before even developing any of the

services for our clients that they have to be thorough with their regulators. So the most important and critical thing is that we ensure to bake the regulators to introduce regulators before we create a whole roadmap of the product. Okay, so that brings more ease and convenience. Yes, the development initiation will take time.

Because when we say that the regulators and compliance are to be involved before defining and setting up how a product should look like. Right. So that needs their legalities, their audit committees and their risk compliance management people to get involved into a product stream as such. But that gives the client as well a very, very thorough and a relief to understand that their product won't get stuck due to any of

the regulatory challenges. This is critically important while you are putting up anything into the market. As I previously mentioned, that trust is the key. And when you are being thorough with the regulatory, you have turned down on all of the safety norms. You have your speed with safety. You have for your innovation done.

for the future, for your digital younger population that you are doing, you are bringing more and more onto the customer convenience. That's what has been a very, very niche focus as of to innovate into the user experience as of now. Those are a couple of achievements that I would say we had been, those are the feathers in our hats as of now.

The reason behind is the clarity of the work that we want to do. So we are thorough and very much clear about how we want to proceed or how we want to take up the quality work that we are delivering. That is what brings in PCA as a trusted partner. Given that.

you work, one of the things that I wanted to pick your mind on was also this that given that you work in multiple geographies.

and you work in multiple industries as well. But even if we just talk about financial services or FinTech, would you be able to give us sort of a state of the sector in the sense that what are some major trends that you see in terms of industry evolution across different geographies? If you could share a few insights on that. Absolutely. So FinTech is evolving.

in a very diversified way across different regions. Every single region is solving a different problem.

For India, the interoperable rails, is UPI, it emerged as the most niche technology that we could deliver. And then it has been enabled, it brought us with instant low cost payments, enabled embedded fintech solutions, which has changed the way e-commerce retail segmentation and others are working.

Everyone would know if you can talk about embedded finance a little bit more. I'll get back to you on this. So all those clubbed together along with the UPI segmentation, this has changed how the business models here are working. Indian business models are now completely dependent on our UPI segmentation. If you look into the African domain,

M-Pesa and Successors, those are the mobile money platforms or mobile money ecosystems that have developed. They lag behind the traditional rails and their focuses are being more on to payments, savings, and microcredits. Now we taken down onto the Latin American portion.

or the Southeast Asian segmentation.

Here, the population has been different. They are emerging with more of the innovation has been focused more on BNPL, that is Buy Now, Pay Later segmentation. Along with it, they have super apps that carry a lot many things altogether. So their focus is absolutely different in terms of their digital population.

we say about fintech, it's not just one thing. There are a lot diversification about the mindset of the people, about the population, their digital understanding, their ecosystems, their culture. And this all comes along with one segmentation, one platform. Now that could be one platform, that could be one super platform or a super application.

that they are doing. when we say about and apart from it, apart from it, this FinTech is still working a lot into CBDC, that is Central Banking Digital Currencies. It is evolving again into cross border transaction trades, which are coming very differently, which is going to reduce down the Forex timings and the Forex charges. So

This is something which was in need of the R to cut down on the monopolized segmentation of the currencies. And along with it, we are transforming fintech.

into more onto now the security segmentation as well. So it's just not about the data regulators or data exchange. Now it is coming more onto the operational security. So we do have a couple of use cases that we handled where the application was being extremely good. The interfaces were being futuristic, but what crashed down was being onto the cyber operational security risk management.

So that is another extremely important thing which requires to be taken care while doing into the fintech. So these are the specific markets that are emerging. would say tokenized liquidity.

is another experimentation along with CBDC that is coming up and I believe we'll soon be able to see new faces of fintech that are coming.

Certainly, so tokenized liquidity is usually worked on across the countries for getting on the payment segmentation. The way we are doing CBDCs, CBDCs would be introduced on one segmentation and tokenized liquidity is for the global transactions. Interesting.

We spoke a little bit about this earlier, but if you can double click on that a little more in terms of... Embedded finances. Embedded finance, I thought I'd take that in little bit, but in terms of balancing between trust and my... So let's say that's the splitting trust on the one side, but then there's also the speed with which I want to build. There's also as an...

I'm incentivized to do things and create experiences that customers or prospects have never seen before. And that means that I'm trying to push boundaries always, which are not necessarily. So I'm reading between the lines in terms of what regulators have said and stuff like that. That's generally, if I'm a founder, if I'm a FinTech company or a product, that's how I think. How do you sort of maintain?

that balance between innovation and building trust and regulators and sort of wanting to do something that's never been done before. That's quite an interesting question because that really needs a lot of brainstorming and there had been times when we could have thought that to give it up.

or to restart it thinking that how to build the whole Lego kind of structure again to see how that works because definitely regulators also keep changing rapidly as the situations are evolving. So when we say about building trust versus innovation, these days, the biggest challenge that we see is

People want to come up with innovation, but that is not solving a problem. Just because it's new doesn't mean it's useful. Exactly. So it's not solving a problem or it's not solving a massive problem. If it is not massive, it is not covering a bigger segmentation. It won't yield you.

And anything that you are doing is not yielding you the revenue that you are expecting will out turn into financially sickness one day or other.

Right? So regulators are there. They are stable. They'll keep changing according to our requirement because the other side, the dark side is also changing every now and then. So they have to be alerted onto the compliance part. And all that is for our safety. All that is for the data safety. And for the innovation segmentation, I always put a hand on it. Yes?

The futuristic ideas are always welcomed, but it need to understand what volume, what mass you would be covering that will be worth of doing all of this assembly together and all the exercises together. So if you're solving a bigger problem, right, that automatically will start building your trust into. Another thing that brings more trust is being disciplined.

Right? Your speed and discipline matters the most. That is something that will come up as your commitment. So commitment is just a word, but the ingredient of it comes with speed and discipline. Interesting. So I think.

I think in some of the things that are currently evolving in the fintech sector, as you also pointed out, one of the things that's been done well is embedded finance. And then the other one that's up and coming or can be seen as a major claim is tokenized liquidity. Can you talk a little bit about embedded finance a little more? Like what is it? Okay. So when we say financial services being threaded with non-financial benefits.

Right? That is what is, that gives your user a more personalized, a more staying onto your services experience. Right? So these days, you'll find competitor to every single service that has been available in the market. Why they choose you?

that's come as embedded services. So for example, insurance at the sales point. You are bringing in more loyalties against the cash rewards. And there are a couple of more, or there are a couple of many such schemes that are being engaged with the credit segmentation as well.

Right. So when you have like payroll integrated with lending system, early salary, stuff like that. Exactly. So those all things are being into the embedded finances.

So like it directly works with my payroll service provider and like if I take out a debt, then the MVFC or whoever is given the debt is able to deduct it directly from my future salaries. That requires a very strong KYC or you can say an automated KYC systems to make sure that your transactions and your services are being secured enough. Yeah, but it's a delight for the user, right?

get the money that I want

so quickly. If I'm not playing foul, which most of us are in, but if I'm not playing foul, then I get the money that I want and then it will be automatically deducted over a period of time. So I don't have to like travel, go to bank, produce papers and stuff like that. It's. So you would see a lot of challenger banking as well. Okay. What is that? Banking services without having physical branches. yeah. Neo banks as they call it. I'm not sure.

terms we call it as Challenger Banking. Now Challenger Banking itself are providing n number of embedded financial services. to make, mean user experience is one of the key factor for any segmentation to be successful. that the ingredients are already discussed through our conversations.

This is super interesting, right? so, but before I let you, I mean, we've spoken about, we've spoken about challenger banking, we've spoken about embedded finance, we've spoken about so many things. Time to sort of try and predict the future. What do you think are going to be some future trends? Who does this industry? If I can ask a real type question.

Who does this industry belong to? Who do you see coming out as? What sort of companies in what sort of geographies do you see coming out as winners in this sector? What should they optimize for? That's quite an interesting thing. I'll be highlighting a couple of pointers that I see would be coming up as the emerging and innovative trends.

And useful, friends. Indeed.

Indeed. to my understanding, CBDC experimentations are definitely going to be the most emerging trend and a lot many things would be revolving around it. The upcoming cross border transaction rates that are getting introduced to see how much innovation convenience is going to get in, that's going to be another one. For example, Europe is

using a very unique segmentation called I-Band.

where all the European banks in any of the given countries the transaction has been as easy as if you are doing an IMPS or an EFT here in India. think so when I get money from outside of India it's an equivalent to Swift like it says Swift slash iBank or something like that. So it's like I can send money from Germany to Spain like I would send money from Mumbai to Bangra.

Okay. So those kind of trends we see that would be evolving in our market as well. Apart from it, we see a lot of things coming up into the cyber security and operational risk segmentation, because without security,

the trust and the data relevancy, the data privacy would not be maintained. And these days, I believe the data is the most critical point to be worked around. Then we see the super applications, right? Which are evolving around the fintech segmentation. So super apps are definitely going to be the future. They will be dominating the market.

And for critical markets like India, which is highly competitive, maintaining those super applications itself is going to be a new innovation. Yeah, it's a present for China. think Elon Musk is trying for it to be a future for US as well through X. It's sort of.

There's a lot of conversation around it, but then it sort of lost its steam. But Super App is...

It is amazing. mean, I was in it's not just in China, the way. It's also in some parts of Southeast Asia as well. When I was visiting and this app is like booking me cabs and getting me food and you know, I'm able to chat with my friends and I'm also like, it's just everything, everything that I do. Absolutely. I can book my concert tickets also. Like it's just

It seemed like they took 10, 12 unicorns in US or India or whatever, and then just put it together and made one happen. Then everyone uses it. I think it's WeChat in China. Yeah, there are a lot many others as well. You'll see Yandex in CIS segmentation. You'll see Grab in Southeast Asian segmentation. yeah.

So India is also evolving. We could see those similar kind of local applications as well who are doing multiple operational challenges. But managing those operational challenges is going to be the innovation.

So the person who can have those kinds of resiliences along with strong operational deliveries. And as we said about, you know, being onto the compliant part as well is going to be the next innovator and winner. Yeah. And they'll also have to build that much trust as well, right? Because across generations, across different avenues of my life, if I'm going to like if me, my kid, my parents are

going to do everything that they do in their life in one app. The amount of trust that that individual or that company will have to build is going to be, I mean, I can't imagine. mean, that's it's exciting. Great. On that note, Pallavi, thank you for for taking on the time and sharing your insights. This has just been our conversation on financial services and fintech.

Given that you are in multiple other sectors as well, I'm sure if you have the time, we'll record another episode some other time in health tech in other sectors as well. But thank you for today. Thank you for joining in. Thank you, Yash. Thank you.

The inbox update you’ll never want to skip

A quick catch-up with ideas, wins, and tips worth stealing, straight to your inbox every week.

The easiest way to reach us.

Share your details and we’ll get back within 24 hours.

Podcast

A plethora of insights,all in one place

From strategy to execution. All the big ideas, practical guides & fresh perspectives that’ll help you scale with confidence

Ebooks

Comprehensive guides that break down the shifts in business and technology, Helping you lead with clarity.

Office Hours

Your direct line to our experts. Practical advice for scaling, right when you need it.

Reports

Data-backed perspectives on where industries are headed, giving you the foresight to make bolder moves.

Newsletter

A quick catch-up with ideas, wins, and tips worth stealing, straight to your inbox every week.

.avif)

Podcasts

Conversations where you get to know everything from the ones who know it best.

.avif)

Hire Offshore Developers, Right Now!

Access top-tier global talent, enterprise infrastructure, and complete regulatory compliance through our proven model.

Start Now